Directly read from a Pandas DataFrame

You can read directly from a Pandas DataFrame. Just give the features/predictors' column names as a list and the target column name as a string to the fit_dataframe method.

At this point, only numerical features/targets are supported but in future releases we will support categorical variables too.

<... obtain a Pandas DataFrame by some processing>

df = pd.DataFrame(...)

feature_cols = ['X1','X2','X3']

target_col = 'output'

model = mlr()

model.fit_dataframe(X=feature_cols,y = target_col,dataframe=df)

Metrics

So far, it looks similar to the linear regression estimator of Scikit-Learn, doesn't it?

Here comes the difference,

Print all kinds of regression model metrics, one by one,

print ("R-squared: ",model.r_squared())

print ("Adjusted R-squared: ",model.adj_r_squared())

print("MSE: ",model.mse())

>> R-squared: 0.8344327025902752

Adjusted R-squared: 0.8100845706182569

MSE: 72.2107655649954

Or, print all the metrics at once!

model.print_metrics()

>> sse: 2888.4306

sst: 17445.6591

mse: 72.2108

r^2: 0.8344

adj_r^2: 0.8101

AIC: 296.6986

BIC: 306.8319

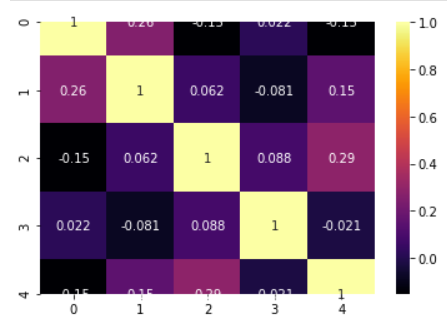

Correlation matrix, heatmap, covariance

We can build the correlation matrix right after ingesting the data. This matrix gives us an indication how much multicollinearity is present among the features/predictors.

Correlation matrix

model.ingest_data(X,y)

model.corrcoef()

>> array([[ 1. , 0.18424447, -0.00207883, 0.144186 , 0.08678109],

[ 0.18424447, 1. , -0.08098705, -0.05782733, 0.19119872],

[-0.00207883, -0.08098705, 1. , 0.03602977, -0.17560097],

[ 0.144186 , -0.05782733, 0.03602977, 1. , 0.05216212],

[ 0.08678109, 0.19119872, -0.17560097, 0.05216212, 1. ]])

Covariance

model.covar()

>> array([[10.28752086, 1.51237819, -0.01770701, 1.47414685, 0.79121778],

[ 1.51237819, 6.54969628, -0.5504233 , -0.47174359, 1.39094876],

[-0.01770701, -0.5504233 , 7.05247111, 0.30499622, -1.32560195],

[ 1.47414685, -0.47174359, 0.30499622, 10.16072256, 0.47264283],

[ 0.79121778, 1.39094876, -1.32560195, 0.47264283, 8.08036806]])

Correlation heatmap

model.corrplot(cmap='inferno',annot=True)

Statistical inference

Perform the F-test of overall significance

It retunrs the F-statistic and the p-value of the test.

If the p-value is a small number you can reject the Null hypothesis that all the regression coefficient is zero. That means a small p-value (generally < 0.01) indicates that the overall regression is statistically significant.

model.ftest()

>> (34.270912591948814, 2.3986657277649282e-12)

How about p-values, t-test statistics, and standard errors of the coefficients?

Standard errors and corresponding t-tests give us the p-values for each regression coefficient, which tells us whether that particular coefficient is statistically significant or not (based on the given data).

print("P-values:",model.pvalues())

print("t-test values:",model.tvalues())

print("Standard errors:",model.std_err())

>> P-values: [8.33674608e-01 3.27039586e-03 3.80572234e-05 2.59322037e-01 9.95094748e-11 2.82226752e-06]

t-test values: [ 0.21161008 3.1641696 -4.73263963 1.14716519 9.18010412 -5.60342256]

Standard errors: [5.69360847 0.47462621 0.59980706 0.56580141 0.47081187 0.5381103 ]

Confidence intervals

model.conf_int()

>> array([[-10.36597959, 12.77562953],

[ 0.53724132, 2.46635435],

[ -4.05762528, -1.61971606],

[ -0.50077913, 1.79891449],

[ 3.36529718, 5.27890687],

[ -4.10883113, -1.92168771]])

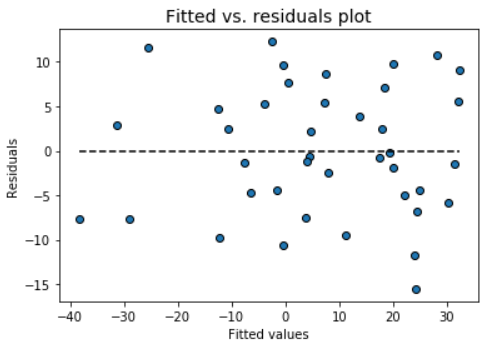

Visual analysis of the residuals

Residual analysis is crucial to check the assumptions of a linear regression model. mlr helps you check those assumption easily by providing straight-forward visual analytis methods for the residuals.

Fitted vs. residuals plot

Check the assumption of constant variance and uncorrelated features (independence) with this plot

model.fitted_vs_residual()

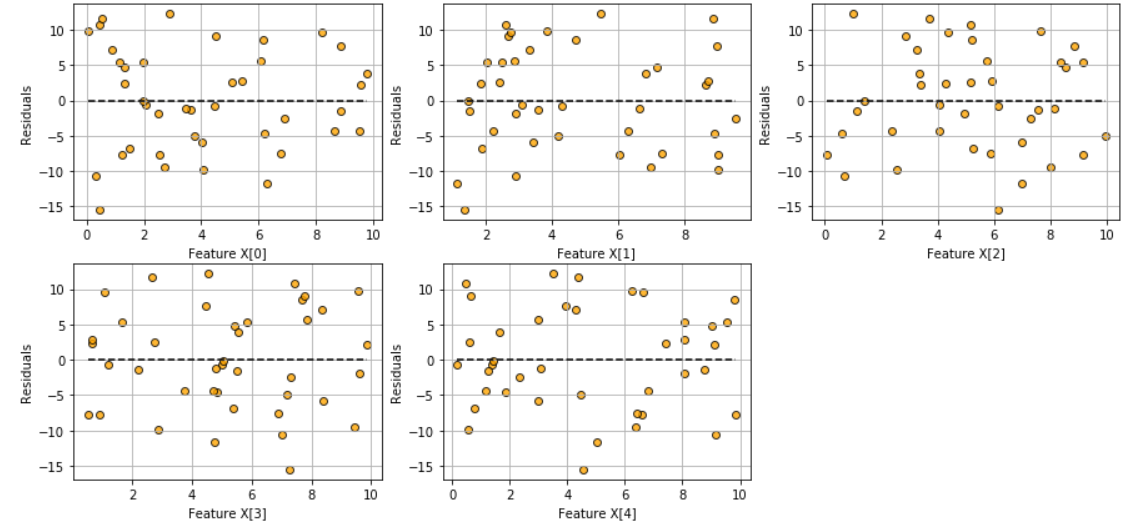

Fitted vs features plot

Check the assumption of linearity with this plot

model.fitted_vs_features()

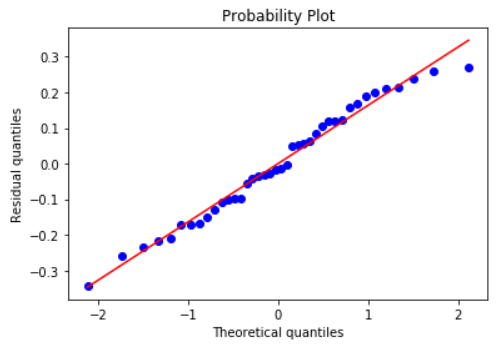

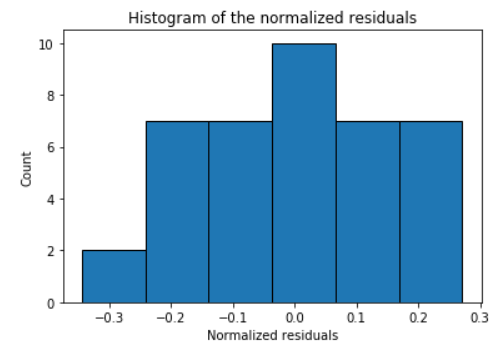

Histogram and Q-Q plot of standardized residuals

Check the normality assumption of the error terms using these plots,

model.histogram_resid()

model.qqplot_resid()